A Guide to Chatbots for Banking in Financial Services

Discover how chatbots for banking are revolutionizing customer service. This guide covers use cases, security, deployment, and choosing the right AI platform.

Banking chatbots are essentially AI-powered assistants, giving customers instant, round-the-clock support for a whole host of financial queries and tasks. You can find them on a bank's website, inside their mobile app, or even on messaging platforms.

Think of them as the new digital front door to the bank. They're designed to handle everything from checking your balance to getting help with a transaction, all without needing a human to step in. For banks, this technology is a game-changer, helping them run more efficiently while satisfying the modern customer's need for "right now" service.

The New Digital Front Door of Banking

Imagine having a personal banker who's always available, speaks your language, and fits in your pocket. That's exactly what banking chatbots are making possible, turning conversational AI into the first point of contact for millions. Banks are jumping on board because, in a digital-first world, nobody has the patience to wait on hold anymore.

This whole shift towards conversational banking is a direct reaction to how customer expectations have evolved. People today, especially younger generations, run their entire lives from their smartphones and they expect their bank to be just as nimble. For routine stuff, a quick text-based chat is far more appealing than a phone call or a trip to a branch. This is where chatbots truly shine, delivering instant answers and carrying out simple commands without any friction.

Why Now Is the Time for AI in Banking

The move to adopt banking chatbots isn't just a local trend; it's a global phenomenon. India, for instance, has become the world’s largest user base for banking chatbots by sheer volume, handling over 250 million chatbot interactions every single month. That massive number really highlights the country's rapid digital sprint in financial services. You can read more about the global rise of banking chatbots and get more insights into adoption statistics.

So, what's driving this? A few key factors are making chatbots an absolute must-have right now:

- Operational Efficiency: Chatbots take care of the common, repetitive questions automatically. This frees up human agents to focus their expertise on the more complex, high-stakes customer problems, which in turn lowers operational costs and makes the entire contact centre more productive.

- Enhanced Customer Experience: Instant answers and 24/7 availability go a long way. This immediate support dramatically improves customer satisfaction and helps build lasting loyalty.

- Data-Driven Personalisation: Every single chat is a source of valuable data. Banks can analyse these conversations to get a much clearer picture of what customers actually need, spot gaps in their services, and start offering truly personalised products and advice.

A well-designed chatbot does more than just answer questions; it becomes a proactive financial assistant. It can alert customers to low balances, flag suspicious transactions, and even offer savings advice based on spending habits.

At the end of the day, banking chatbots are no longer a "nice-to-have" innovation; they are a core part of modern banking. This guide will walk you through everything, from their practical uses in customer support to the crucial security and compliance layers that make them work. We'll give you a complete picture for building a smarter, more responsive digital bank for your customers.

How Chatbots Are Redefining Banking Operations

It’s easy to think of chatbots as simple FAQ tools, but in banking, they’ve grown into something far more significant. They're now a tireless digital workforce, reshaping everything from how a customer interacts with their account to how bank employees get their jobs done.

Chatbots have moved well beyond basic Q&A. They now handle complex tasks that directly influence customer satisfaction and free up human teams to focus on more complex work. We’re seeing their value emerge on two major fronts: enhancing the customer experience and streamlining the bank's own internal processes.

For customers, this means getting answers and services without the old frustrations of call queues or trekking to a branch. This kind of instant support isn't just a bonus anymore; it's what people expect. Just look at the results from Indian banks, where chatbots are already handling 87% of banking inquiries in under 60 seconds without any human intervention. You can dig into more stats on chatbot adoption in banking on sqmagazine.co.uk.

That single statistic says it all. These aren't just tools for cutting costs. They're actively making banking faster and better.

Elevating the Customer Experience

From the customer's perspective, a good banking chatbot feels like having a personal financial assistant on call, 24/7. It takes the friction out of everyday banking, turning what used to be chores into simple, quick conversations.

Think about these real-world scenarios:

-

Instant Account Services: Instead of fumbling through an app menu, a customer can just type, "What's my account balance?" or "Show me my last five transactions." The chatbot securely authenticates them and pulls up the information in seconds. A multi-step task becomes a single sentence.

-

Streamlined Lead Generation: Someone browsing your website is curious about a home loan. The chatbot can pop up, ask a few qualifying questions, collect their details, and even offer to schedule a call with a mortgage advisor. The lead is captured and nurtured on the spot.

-

24/7 Transaction Support: A customer notices a strange charge on their card late at night or loses their wallet on a bank holiday. A chatbot can immediately start the process to dispute the charge or block the card, providing instant peace of mind and preventing fraud.

By taking care of these high-volume, straightforward requests, chatbots do more than just make customers happy. They also generate a goldmine of data. Banks can analyse these conversations to pinpoint common frustrations and spot opportunities for new services.

This kind of proactive, always-on support is key to building loyalty. It shows the bank respects its customers' time and is there for them whenever they're needed.

Empowering Internal Banking Teams

The impact of banking chatbots doesn't stop with the customer. They're also becoming incredibly powerful tools behind the scenes, helping employees find information and work more efficiently. This internal boost is just as vital to a bank's overall performance.

Internally, these AI assistants act like a central brain for the organisation. They're a knowledge hub and an automation engine rolled into one, cutting down on administrative headaches so specialist staff can focus on what they do best.

Here's how they're making a difference for the team:

-

Instant Policy and Procedure Access: A loan officer needs to double-check a specific compliance rule. Rather than digging through a clunky intranet, they can ask the internal bot a direct question and get an immediate, accurate answer. This ensures everyone is consistent and follows the rules.

-

Automated IT and HR Support: Think about all the simple, repetitive questions HR and IT get every day. Password resets, requests for new equipment, or questions about leave policy can all be handled by a bot. This frees up the IT and HR teams for more strategic work.

-

Onboarding and Training: For a new employee, a chatbot can be an interactive guide to the company. It can answer questions about systems, company culture, and job-specific processes, offering consistent support from their very first day.

When you automate these internal jobs, you create a sharper, more knowledgeable workforce. And that internal efficiency always circles back to the customer, because a well-supported employee is far better equipped to provide great service.

Building Trust with Secure and Compliant AI

In finance, trust isn't a nice-to-have; it's the bedrock of your relationship with your customers. When you bring a chatbot into the mix, security and compliance can't be an afterthought. They have to be baked in from the very beginning. Customers need to know, without a shadow of a doubt, that their sensitive financial information is safe with every single tap and keystroke.

Think of it this way: your digital assistant needs to be built like a fortress. The entire point is to make chatting with your bank just as secure—if not more so—than logging into your online banking portal. Every single message, from a simple balance check to a request to transfer funds, has to be completely shielded from prying eyes.

Fortifying Conversations with Core Security Protocols

To get that level of security, you need multiple layers of protection working together. It’s a bit like a bank vault with several different locks. Each security measure is another barrier, making sure only the right person gets access to their information. This multi-layered approach is critical for protecting data whether it's sitting on a server or zipping across the internet.

Here are the non-negotiables for any banking chatbot:

- End-to-End Encryption: This is the digital equivalent of a sealed, tamper-proof envelope. It scrambles the conversation between the customer and the chatbot, making it completely unreadable to anyone trying to intercept it.

- Multi-Factor Authentication (MFA) Integration: For any serious action, like moving money or updating personal details, the chatbot absolutely must trigger an MFA prompt. This might be a one-time password (OTP) sent to the customer’s phone or a quick fingerprint scan, adding that crucial second layer of verification.

- Secure API Gateways: Your chatbot needs to talk to the bank's core systems to get information. Secure API gateways act as the bouncers at the door, strictly managing these connections, enforcing access rules, and keeping a detailed log of every request to block any unauthorised activity.

These safeguards are the technical foundation of a chatbot people can trust. They work quietly in the background to keep every conversation private and secure.

Navigating the Regulatory Maze

Beyond the tech, banking chatbots have to play by the rules—a complex web of financial regulations. This isn't just about ticking boxes. It's about showing a real commitment to protecting your customers' data and their rights. In India, for instance, banks must follow strict guidelines from the Reserve Bank of India (RBI) on everything from where data is stored to how consumer complaints are handled.

A compliant chatbot is designed with privacy at its core. It must ensure that all customer data is handled in accordance with prevailing laws, such as rules around data storage, consent management, and the right to data erasure.

Getting this wrong is a huge risk. We're talking about hefty fines and, worse, a complete collapse of customer trust that could take years to rebuild. That’s why the chatbot platform itself must have features like detailed audit trails that log every interaction for review and role-based access controls, making sure only specific, authorised bank staff can see sensitive conversation data. This obsessive attention to detail is essential.

Turning AI into a Proactive Defence

Modern AI is more than just a conversationalist; it can be your first line of defence against fraud. By analysing conversation patterns in real-time, these systems can spot unusual behaviour that might signal something is wrong.

For example, a smart chatbot can pick up on and flag suspicious activity like:

- Someone trying to log in from an unusual location or at a strange time.

- Quick, repeated attempts to get sensitive information.

- Phrases and patterns that look like common social engineering or phishing tactics.

When the AI spots a potential threat, it can instantly hand the conversation over to a human fraud expert or even temporarily lock the account to stop a suspicious transaction in its tracks. This turns the chatbots for banking from a simple service tool into a vigilant, 24/7 security guard, actively protecting both the customer and the bank from financial crime.

Architecting a Scalable Banking Chatbot System

To really get a feel for what makes a banking chatbot effective, you have to look under the bonnet at its technical architecture. It's far more than a simple Q&A tool. A truly robust chatbot is a complex system of interconnected parts, all designed for top-notch security, scalability, and a smooth user experience. Building one successfully isn't just about scripting conversations; it's about engineering a resilient digital assistant that can grow right alongside your bank.

Think of the architecture as the backstage crew for a conversation. When a customer pings a message, a series of quick, precise handoffs happen in the background. Each component has a specific job, making sure the query is understood, the right information is found, and a helpful response is sent back—all in a matter of seconds.

This whole process relies on several core layers working in perfect sync. The engine that understands human language is at the heart of it, but its true power is only unleashed when it’s securely plugged into the bank's core systems.

The Core Components of a Banking Chatbot

A well-designed banking chatbot is built on three fundamental pillars. Each plays a distinct role in turning a simple text message into a successful banking action, from figuring out the initial request to delivering a final, accurate answer.

-

Natural Language Processing (NLP) Engine: This is the chatbot's brain. It takes what the customer types—whether it's "check my balance" or "how much did I spend on groceries last week?"—and figures out the intent. It’s the part that understands slang, typos, and all the different ways people can ask for the same thing.

-

Dialogue Manager: Once the NLP engine knows what the customer wants, the dialogue manager steps in. It acts as the conversation's director, deciding the next logical step. It might ask for more detail ("Which account would you like to check?"), walk the user through a process, or realise it needs to fetch some data from another system.

-

Integration Layer: This is the critical bridge connecting the chatbot to the bank's existing infrastructure. Using secure Application Programming Interfaces (APIs), this layer lets the chatbot talk to core banking systems, Customer Relationship Management (CRM) platforms, and other key databases to pull real-time, personalised information.

Without this tight integration, a chatbot is little more than an interactive FAQ page. It’s the ability to connect securely to backend systems that transforms it into a powerful tool for day-to-day banking.

Securely Connecting to Core Banking Systems

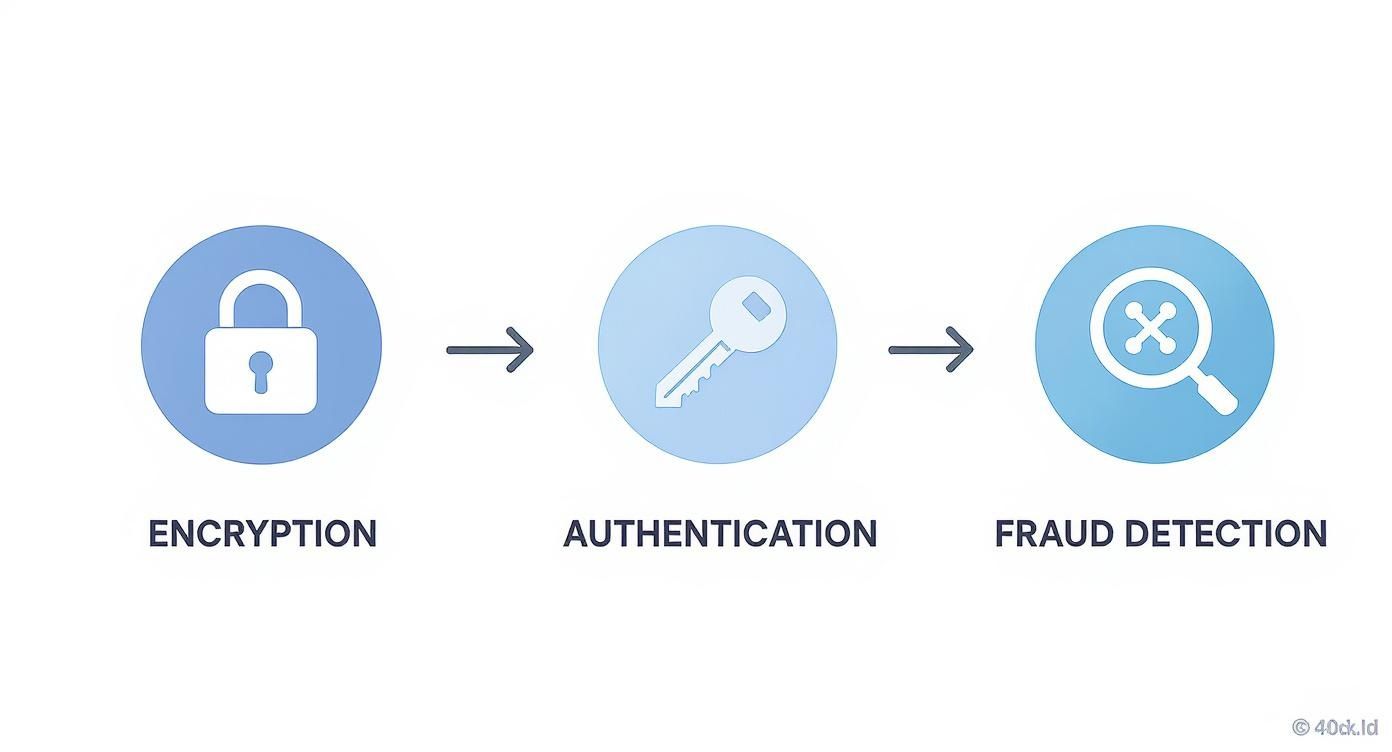

The integration layer is where security really comes into focus. A chatbot needs to access sensitive customer data, so this connection has to be ironclad against any potential threats. This is done using secure API gateways, which act as vigilant gatekeepers, managing and monitoring every single request the chatbot sends to internal systems.

The visual below shows how security protocols like encryption and authentication form a critical chain of defence for every interaction.

This flow makes it clear that every conversation is shielded by multiple layers of protection. Data is encrypted while in transit, and the user is properly authenticated before any sensitive action is taken.

A scalable architecture isn't just about handling more users; it's about maintaining airtight security as the system grows. Each new feature or integration must adhere to the same strict security standards as the core system.

The Hybrid Model and Smart Escalation

Let's be realistic—even the most advanced AI will run into questions it can't answer. This is where a hybrid model is essential for a great customer experience. Instead of the chatbot hitting a dead end, there needs to be a clear, context-aware process for handing the conversation over to a human agent.

This isn't just about a simple transfer. A well-built system makes sure all the relevant context—the customer's identity, the chat history, and the specific problem they're facing—is passed directly to the agent. This means the customer never has to repeat themselves, which turns a potential frustration into a smooth, efficient resolution.

Platforms like SupportGPT are designed for this kind of smart escalation, using natural-language rules to ensure a graceful handoff that keeps the customer experience intact. This approach creates a resilient system that's truly built for future growth.

Measuring the Real ROI of Your Chatbot

https://www.youtube.com/embed/H-xQZz-RbHI

So, you've deployed a banking chatbot. That's a big step, but how do you prove it’s actually working and not just a flashy new toy? The secret is looking beyond simple vanity metrics, like the total number of conversations. To get the real picture, you need to focus on Key Performance Indicators (KPIs) that show a tangible impact on your business.

A solid measurement framework helps you track the real-world return on your investment in conversational AI. We can break this down into three core areas that every banking leader cares about: operational efficiency, customer satisfaction, and direct business value. Each one tells a crucial part of your chatbot's success story, from cutting costs in your contact centre to building customer loyalty and even driving revenue.

This kind of data-backed approach is more important than ever. The conversational AI market in India’s financial sector, currently valued at INR 38.10 billion, is expected to explode to INR 152.31 billion by 2030. That’s a compound annual growth rate of about 26.22%. This growth is happening because banks are realising how much AI chatbots can improve efficiency and customer experience. You can discover more about this market growth on BusinessWire.

To help you get started, here’s a look at the essential KPIs you should be tracking to measure the performance and business impact of your banking chatbot.

Key Performance Indicators for Banking Chatbot Success

| KPI Category | Metric | What It Measures |

|---|---|---|

| Operational Efficiency | Containment Rate | The percentage of chats fully handled by the bot without human help. |

| First-Contact Resolution (FCR) | The percentage of issues solved in the very first interaction with the bot. | |

| Average Handling Time (AHT) | How quickly the bot resolves a typical query compared to a human agent. | |

| Customer Satisfaction | Customer Satisfaction (CSAT) Score | Direct feedback on how happy customers are with their chatbot interaction. |

| Net Promoter Score (NPS) | Customer loyalty and willingness to recommend your bank based on the experience. | |

| User Retention Rate | How many customers return to use the chatbot for future queries. | |

| Business Value | Lead Conversion Rate | The bot's success in turning a query into a qualified lead for a product. |

| Product Cross-sells | How often the bot successfully suggests and interests users in other products. | |

| Cost Savings | The total reduction in operational costs from deflected calls and agent time. |

By tracking a balanced mix of these metrics, you can build a comprehensive view of your chatbot's performance and confidently demonstrate its value to the entire organisation.

KPIs for Operational Efficiency

The first place you’ll see your chatbot making a difference is in your daily operations. These metrics are all about how well your bot is taking routine, repetitive tasks off your team's plate, freeing them up to handle the trickier stuff.

-

Containment Rate: Think of this as your bot's independence score. It measures the percentage of conversations the chatbot resolves all on its own, without ever needing to escalate to a human agent. A high containment rate is a direct sign that your bot is effective and is saving you money.

-

First-Contact Resolution (FCR): This one is crucial. It tells you how many customer problems are completely solved in their first interaction with the chatbot. A high FCR means your bot isn't just giving generic answers; it's providing accurate, complete solutions that stop customers from having to call or email in.

These two KPIs are your proof that the chatbot is successfully deflecting queries from your human support teams, which is often the biggest driver of ROI.

Gauging Customer Satisfaction

Efficiency is great, but it’s worthless if your customers hate using the chatbot. Tracking satisfaction metrics ensures that your technology is actually helping people and building stronger relationships, not creating frustration.

A chatbot should make banking easier, not more frustrating. Measuring customer sentiment directly is the only way to ensure your technology is truly helping, not hindering, the customer journey.

A few key metrics to watch here include:

-

Customer Satisfaction (CSAT) Score: This is as simple as it gets. After a chat, you ask customers to rate their experience. A consistently high or rising CSAT score is a clear signal that your chatbot is hitting the mark.

-

User Retention Rate: This KPI shows you how many customers come back to use the chatbot a second, third, or fourth time. High retention is a great sign that people find it a genuinely useful and reliable way to manage their banking needs.

Tracking Direct Business Value

Finally, the most advanced chatbots for banking go beyond support; they actively contribute to your bottom line. These are the metrics that connect your chatbot’s performance directly to revenue and sales.

For example, tracking lead conversion rates shows you how good the chatbot is at identifying potential customers for loans, credit cards, or investment products and then passing them on to the right team. In the same way, measuring product cross-sells proves its ability to make smart, relevant recommendations based on what it knows about the customer. These are the KPIs that turn your chatbot from a cost centre into a powerful revenue-generating asset.

How to Choose the Right Chatbot Platform

Picking a technology partner is a huge decision. It's one that will define your digital customer experience for years to come, so it’s worth getting right. The market is crowded, but if you have a solid evaluation framework, you can cut through the noise and find a platform that truly fits your bank's needs—especially around security, integration, and where you want to go in the future.

The first big choice is whether to build a custom solution from scratch or go with an established, enterprise-ready platform. Building in-house gives you total control, but it's a massive undertaking. We're talking about a steep learning curve, a hefty upfront investment, and a long, drawn-out development timeline.

Key Evaluation Criteria for Vendors

For most banks and financial institutions, partnering with a specialised platform is simply the more practical path. These solutions arrive with essential banking features already built-in, which slashes your implementation time and reduces a lot of the risk.

As you start looking at different vendors, here are the absolute must-haves to focus on.

-

Security and Compliance Certifications: Don't even consider a vendor without industry-standard certifications like ISO 27001 and SOC 2. These aren't just fancy acronyms; they're hard proof that the platform has passed rigorous, independent audits of its security controls. This is non-negotiable when you're handling sensitive financial data.

-

Proven Integration Capabilities: A chatbot is useless if it can't talk to your other systems. The platform needs to have robust, secure APIs that can plug seamlessly into your core banking systems, CRM, and any other software you rely on. Always ask for case studies showing successful integrations with institutions like yours.

-

Advanced Analytics and Reporting: You have to be able to see what's working and what isn't. A good platform will give you a detailed analytics dashboard to track everything from containment rates to customer satisfaction scores. This is how you'll measure your return on investment and find ways to keep making the experience better.

Why Specialised Platforms Outperform Generic Tools

Generic chatbot builders can look tempting at first, but they almost always fall short because they're missing the specific features that are critical for banking. An enterprise platform designed for support automation, on the other hand, comes with these functionalities ready to go, saving you a ton of development work and keeping you compliant from the start.

Look for platforms that offer:

- Comprehensive Audit Trails: You need the ability to log every single interaction and system change. It’s essential for regulatory reviews and internal governance.

- Role-Based Access Controls (RBAC): This feature is key for making sure only authorised staff can access sensitive customer conversations or tweak the chatbot's settings.

Choosing a platform is about more than just the tech. It’s about finding a partner who genuinely understands the unique pressures and demands of the financial world. A platform with security and compliance baked in gives you the freedom to innovate with confidence.

For example, platforms like SupportGPT are specifically engineered with enterprise-grade security and smart escalation logic, built to handle the distinct challenges of financial services. When you pick a partner who already has a deep understanding of banking, you can deploy powerful chatbots for banking that not only meet what customers expect today but also give you a solid foundation to build on for years to come.

Answering the Big Questions About Banking Chatbots

Bringing any new technology into a bank naturally comes with a healthy dose of scrutiny. When it comes to chatbots, leaders are right to ask tough questions about security, the impact on their teams, and what it really takes to get one up and running. Getting clear, honest answers to these concerns is the first step toward a successful rollout.

Let's tackle the most common questions we hear from financial institutions weighing up conversational AI.

Is Customer Data Genuinely Secure with a Chatbot?

This is usually the first and most important question asked, and rightly so. The short answer is yes, but only if the platform is built with a security-first mindset. A top-tier chatbot for banking isn't just a simple chat window; it's a fortress of security measures.

We're talking about end-to-end encryption for every single message, secure API gateways for any communication with your core banking systems, and mandatory Multi-Factor Authentication (MFA) before any sensitive action is authorised. Think of it less like a website chat and more like an extension of your secure online banking portal. The platform itself should also be backed by certifications like ISO 27001, which is the gold standard for information security management.

Will a Chatbot Make Our Human Agents Redundant?

This is a very common fear, but it's based on a misunderstanding of what these bots are designed to do. The goal isn't replacement; it's elevation. Chatbots excel at handling the high-volume, predictable queries that often overwhelm support teams—things like "What's my balance?", "Show me my last five transactions," or "What are your opening hours?".

By automating these routine tasks, you get two massive benefits:

- Instant answers for customers: They get what they need immediately, 24/7, without waiting in a queue.

- Empowered agents: Your human experts are freed from repetitive work. They can now dedicate their time and skills to complex, high-value conversations that truly require a human touch, like handling a fraud claim or offering personalised financial advice.

The best approach is a partnership model. The chatbot serves as the first point of contact, handling the simple stuff and seamlessly handing the conversation over to a human agent—with full context—the moment a query gets too complex or the customer asks for a person.

How Long Does It Actually Take to Implement a Banking Chatbot?

This is where people are often pleasantly surprised. If you're imagining a multi-year IT project, think again. While building a custom solution from the ground up can indeed take over a year, deploying a chatbot using a specialised enterprise platform is a matter of weeks or a couple of months.

The process is much more straightforward:

- First, we pinpoint the initial use cases that will deliver the most value, like automating FAQs or enabling balance checks.

- Next, the AI is trained on your bank's specific knowledge base, products, and policies.

- We then securely connect the bot to your core systems through APIs.

- Finally, we go through a phase of rigorous testing and refinement before going live.

Modern platforms are built for speed, meaning you can start seeing a real return on your investment much, much faster.

Ready to see how a secure, intelligent AI assistant can transform your customer support? SupportGPT offers an enterprise-grade platform to build and deploy powerful chatbots for banking, complete with advanced security, smart escalation, and deep analytics. Start your free trial today.